Altseason Coming in 2025? Cycles, Indicators, and Macro Dynamics

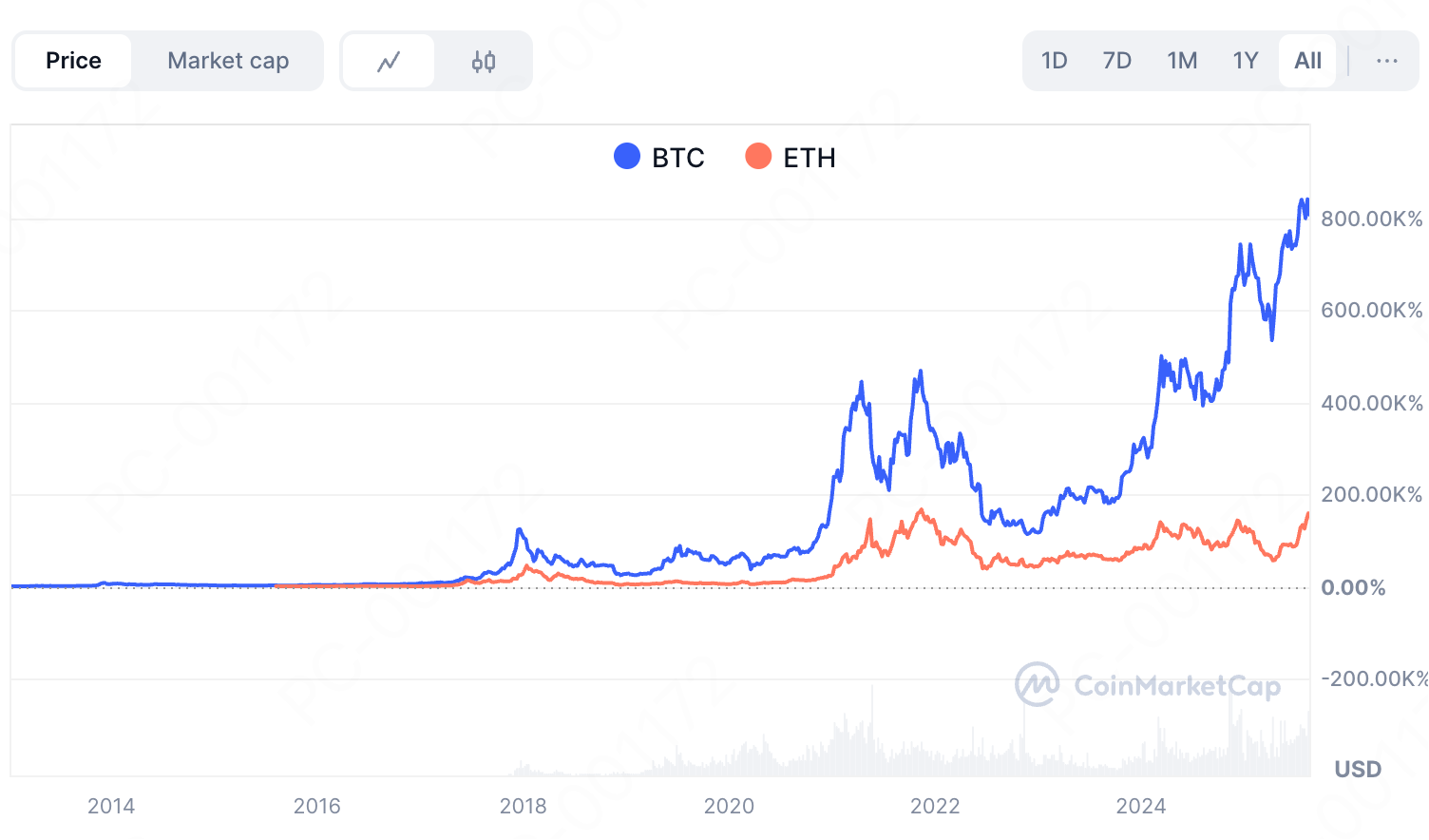

1. Historical Pattern Comparison: Classic Cycles vs. Current Differences

1.1 The "Three-Stage" Rule of Classic Cycles

- BitcoinDominance Stage: Bitcoin, as the market leader, first attracts a large amount of liquidity, driving its price sharply upward.

- Ethereum and Large-Cap Altcoin Stage: When Bitcoin's rally slows, market funds start seeking new opportunities. Ethereum, thanks to its position in smart contracts and the DeFi ecosystem, becomes the main beneficiary. At the same time, some large-cap altcoins also perform strongly.

- Mid- and Small-Cap Altcoin Frenzy Stage: Market sentiment reaches its peak, and funds—with risk appetite fully unleashed—flow into smaller-cap assets, bringing returns of tens to even hundreds of times, forming the so-called "altseason."

1.2 Differences Between the Current Market and Historical Patterns

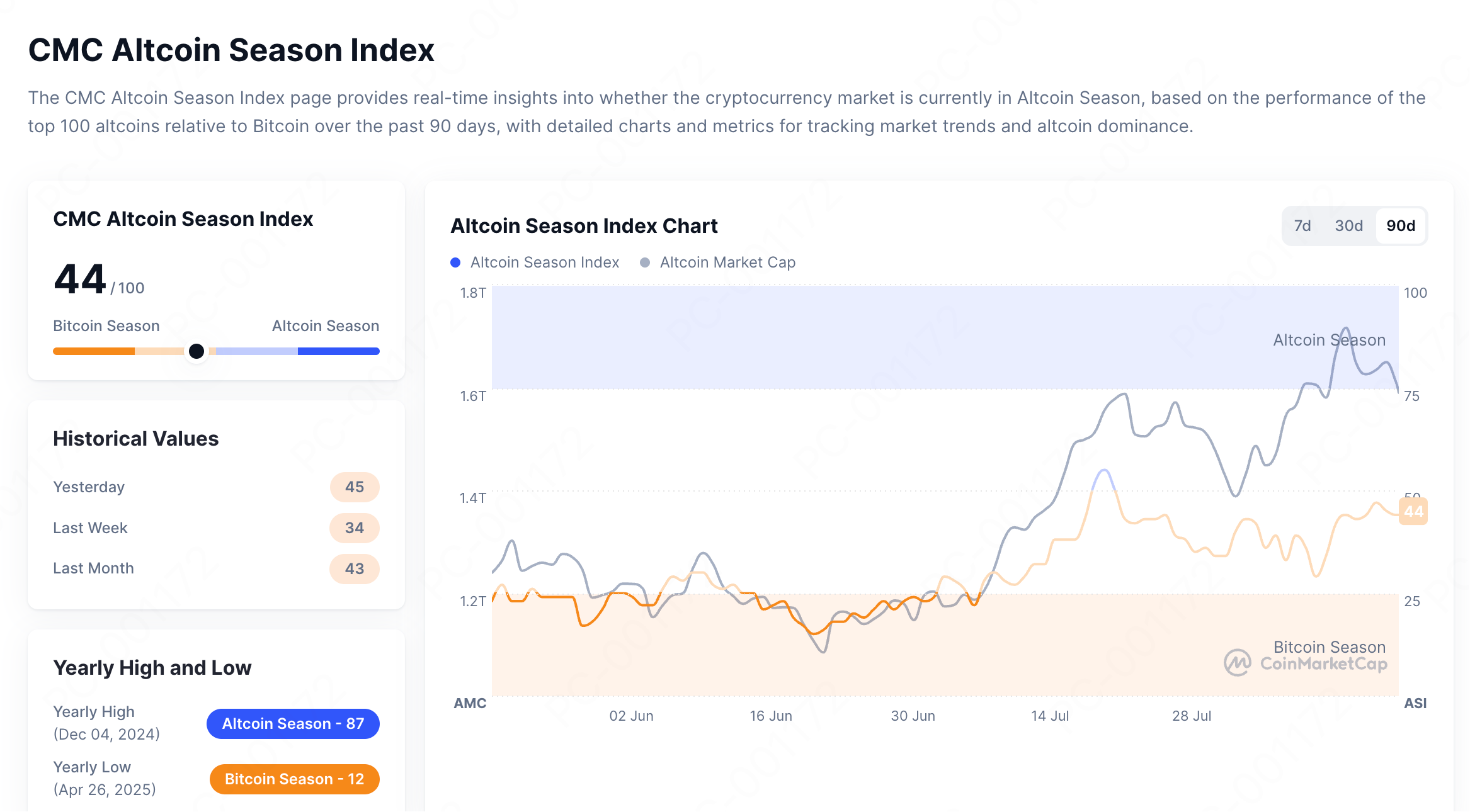

2. Key Indicator Analysis: Potential Altcoin Season Signals

2.1 Bitcoin Dominance

2.2 Altcoin Season Index

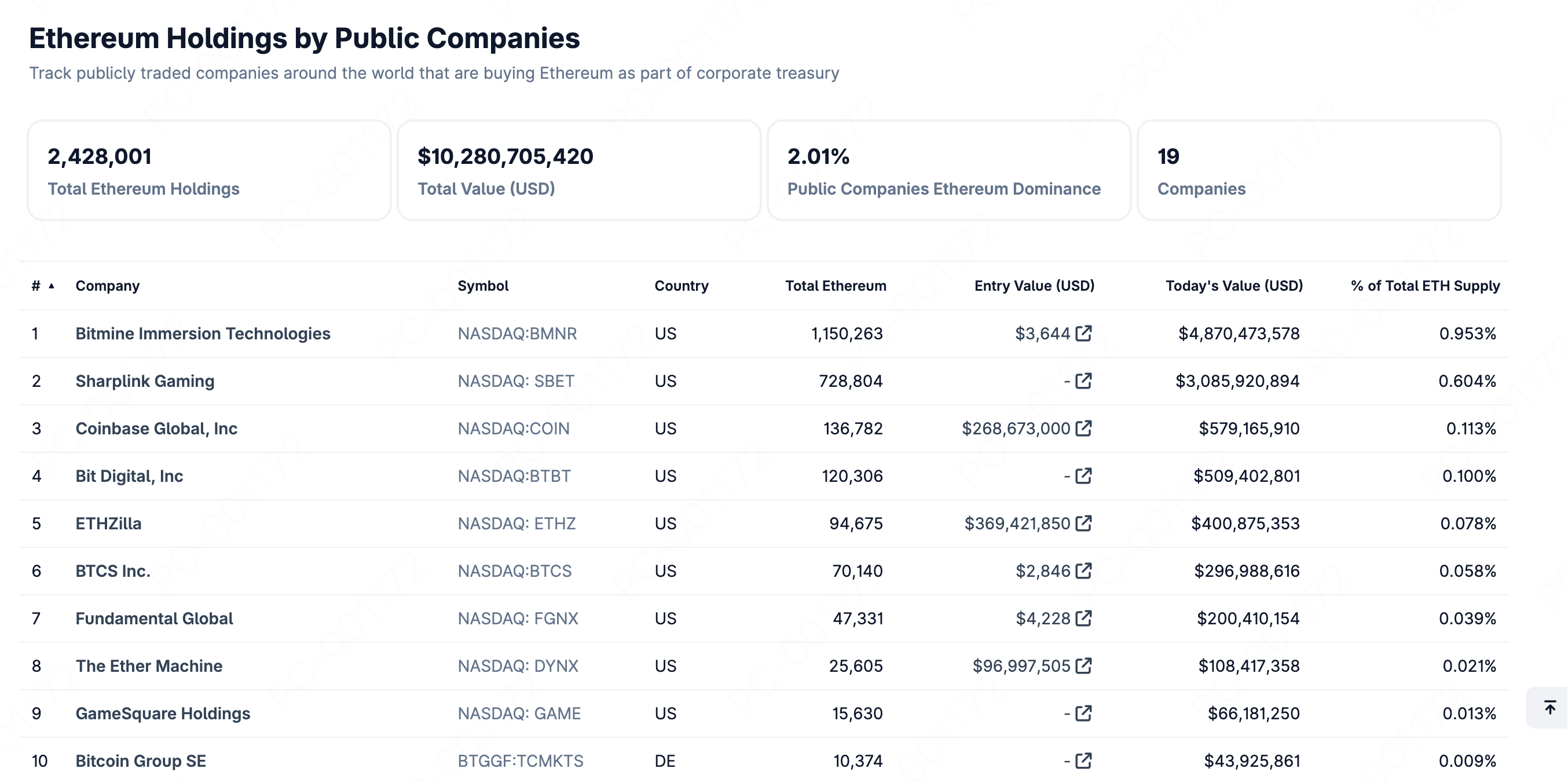

3. Institutional Behavior and Macroeconomic Policies: Catalysts for Altcoin Season

3.1 Institutional Capital Participation

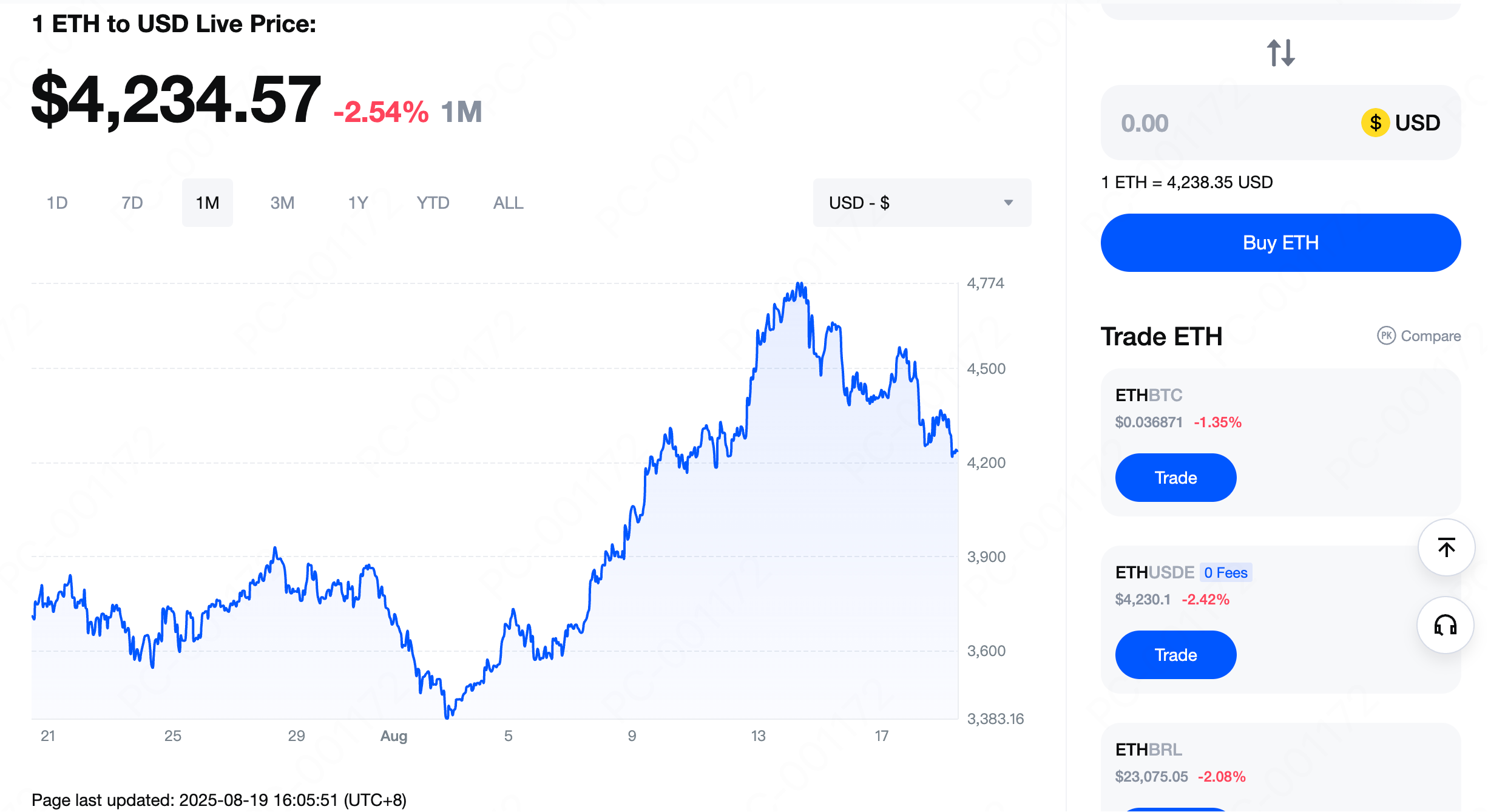

3.2 Macroeconomic Policies and Liquidity Changes

4. Second-Half Outlook: Potential Paths for Altcoin Season

5. Conclusion: Measured Optimism, Rational Positioning

Popular Articles

MEXC Account Problems Solved: Login Issues, KYC, Withdrawal & Support Guide

1. Login1.1 How do Ilog inwhen neither mymobilenumber noremail are accessible?If you remember your account login password:On the Web: On the official login page, enter your account and password, then

How to Send Bitcoin? Complete Step-by-Step Guide

Sending bitcoin might seem complicated at first, but it's actually straightforward once you understand the basics.This guide walks you through everything you need to know about how to send bitcoin saf

Bitcoin vs Gold: Which Asset Wins as a Store of Value?

The debate between bitcoin vs gold has intensified as both assets reach historic valuations in 2025. Gold has surged significantly with prices above $3,000 per ounce while Bitcoin trades above $100,00

Why Is Bitcoin Valuable? 5 Key Reasons Behind Its Price

Bitcoin has climbed from pennies to tens of thousands of dollars, yet many still wonder how digital currency without physical backing holds any value. This article explains the core factors that make

Hot Crypto Updates

Beeg Blue Whale (BEEG) Community Culture & Meme Economics Deep Analysis

Executive Summary Beeg Blue Whale (BEEG) is more than just a cryptocurrency token—it's an extension of internet meme culture into the blockchain realm. This article explores BEEG community cultural ch

Beeg Blue Whale (BEEG) Price Prediction 2025-2030: Worth Investing?

Executive Summary Beeg Blue Whale (BEEG) currently trades around $0.000024, down 98% from May 2025 all-time high of $0.001193. This article combines technical analysis, fundamental assessment, and mar

Beeg Blue Whale (BEEG) Complete Beginner's Buying Guide: Investing in BEEG from Scratch

Executive Summary For newcomers to cryptocurrency, purchasing Beeg Blue Whale (BEEG) may seem complex, but actually requires just a few simple steps. This guide starts from zero, detailing how to safe

2026 Meme Coin Investment Strategy Complete Guide: Beeg Blue Whale (BEEG) Case Study

Executive Summary The 2026 meme coin market has surpassed $100 billion in total value, but successful investment requires more than luck—it demands systematic strategy. This article uses Beeg Blue Wha

Trending News

MAXI DOGE Holders Diversify into $GGs for Fast-Growth 2025 Crypto Presale Opportunities

Presale crypto tokens have become some of the most active areas in Web3, offering early access to projects that blend culture, finance, and technology. Investors are constantly searching for the best

Bank of Canada cuts rate to 2.5% as tariffs and weak hiring hit economy

The Bank of Canada lowered its overnight rate to 2.5% on Wednesday, responding to mounting economic damage from US tariffs and a slowdown in hiring. The quarter-point cut was the first since March and

The Daily: Upbit flags private key vulnerability, MegaETH to return funds from pre-deposit campaign, Do Kwon requests 5-year jail cap, and more

The following article is adapted from The Block’s newsletter, The Daily, which comes out on weekday afternoons.

Surprising Shifts in Bitcoin’s Fortunes Amid Global Political Tensions

The post Surprising Shifts in Bitcoin’s Fortunes Amid Global Political Tensions appeared on BitcoinEthereumNews.com. The cryptocurrency realm is witnessing substantial fluctuations with Bitcoin‘s valu

Related Articles

What is Chiliz (CHZ)? The World's First Blockchain for Sports and Entertainment

TL;DR1) Professional Positioning: Chiliz Chain is the world's first blockchain dedicated to sports and entertainment, partnering with over 70 elite sports teams worldwide.2) Fan Token Innovation: Thro

What is Ethena? A Complete Guide to the Crypto-Native Synthetic Dollar Protocol

TL;DR1) USDe is a synthetic dollar, not a fiat-backed stablecoin: It is backed by crypto assets and corresponding short futures positions instead of traditional fiat reserves.2) Delta-hedging ensures

What Are Fan Tokens? 80 Tokens Connecting Global Fans with Over $52 Million in Daily Trading Volume

Discover Fan Tokens Backed by Sports Giants on MEXC: Major Events Now LiveFan tokens are the official digital asset class for sport. Created on Chiliz Chain, powered by CHZ, and launched by the bigges

What is JESSE? An In-Depth Analysis of the Decentralized Content Coin Launched by Base Core Developer

Key Highlights 1) JESSE is a personal token created by Jesse Pollak, a core developer of the Base network. 2) Positioned as a "Content Coin," JESSE establishes direct connections between creat