Tesla Stock Price Prediction: Why The EV Maker Is Sitting Right at Fair Value

The post Tesla Stock Price Prediction: Why The EV Maker Is Sitting Right at Fair Value appeared first on 24/7 Wall St..

Tesla (NASDAQ:TSLA) has been one of 2026’s most-debated stocks, swinging between SpaceX-merger fever and valuation skepticism. After running the numbers, our 24/7 Wall St. price target lands almost exactly where shares trade today, with a modest single-digit upside that earns a buy rating but stops well short of a table-pounding call.

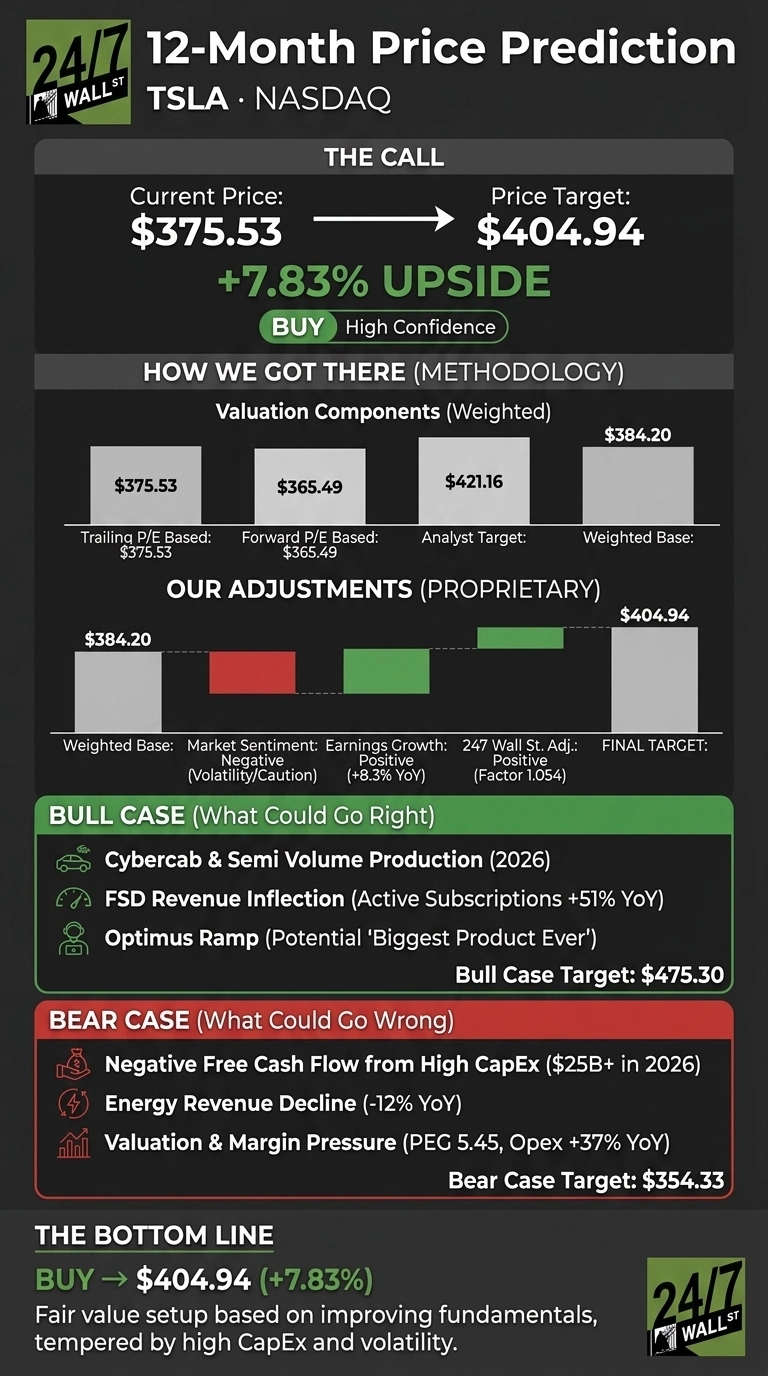

Tesla closed at $375.53 on June 24, 2026. Our 24/7 Wall St. price target for Tesla is $404.94, implying 7.83% upside over the next 12 months. We rate the stock a buy with high confidence, but call this a fair-value setup rather than a deep discount.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $375.53 |

| 24/7 Wall St. Price Target | $404.94 |

| Upside | 7.83% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Rough Six Months Sets the Stage

Tesla has cooled meaningfully in 2026. Shares are down 16.5% year to date, off 11.85% over the past month, and sit roughly 16% below the $498.83 52-week high (low of $288.77).

Yet fundamentals are improving. Q1 2026 delivered $22.39 billion in revenue, up 15.8% YoY, with non-GAAP EPS of $0.41 beating consensus by 17.78%. Automotive gross margin expanded to 21.1% from 16.2%, FCF climbed 117.47% to $1.44 billion, and active FSD subscriptions hit 1.28 million, up 51% YoY.

The Case for $475 and Beyond

Bulls have a real story. Management committed to over $25 billion in 2026 CapEx to fund Cybercab, Tesla Semi, Megapack 3, the Optimus ramp, AI5 silicon, and the new semiconductor research fab in Austin. CFO Vaibhav Taneja called it the “right strategy to position the company for the next era.” Barclays has an equal weight rating on the shares with a $360 price target.

Elon Musk argued Optimus could be “the biggest product ever” and guided unsupervised FSD for customer cars by Q4 2026. Wall Street’s average analyst target sits at $421.16, with 23 Buy ratings against 7 Sells. Our bull-case scenario gets shares to $475.30, a 26.57% return, if Cybercab, Robotaxi expansion, and Optimus convert the AI narrative into revenue.

What Could Go Wrong

The bear case starts with valuation. Tesla trades at a 344 trailing P/E and 192 forward P/E, with a PEG of 5.45. Energy revenue fell 12% YoY, opex jumped 37%, and management openly guided for negative free cash flow the rest of 2026. Insider direction is net selling on 49 recent transactions.

Counterfactually, the opex spike reflects AI5 chip development and the CEO award SBC, both arguably investments in long-duration optionality rather than operating decay. Still, our bear scenario maps to $354.33, a 5.65% drawdown.

The Bottom Line: A Fair-Value BUY

My 24/7 Wall St. price target of $404.94 reflects a stock priced almost exactly where the fundamentals justify, with our 247Factor providing the tiebreaker. The bull thesis depends on Cybercab volume production and FSD revenue inflecting in late 2026 as guided.

The bear case hinges on the $25 billion CapEx cycle pressuring margins faster than AI revenue can offset. With 90% confidence, this is a modest buy, not a conviction call.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $404.94 |

| 2027 | $430.45 |

| 2028 | $457.55 |

| 2029 | $483.20 |

| 2030 | $509.74 |

These projections assume Tesla executes the Cybercab, Optimus, and FSD roadmap on management’s timeline. Significant upside or downside could come from China FSD approval, the SpaceX equity relationship, or a sharper-than-expected demand softness in the core auto business.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Tesla didn’t make the cut. Grab the names FREE today.

The post Tesla Stock Price Prediction: Why The EV Maker Is Sitting Right at Fair Value appeared first on 24/7 Wall St..

You May Also Like

AI predicts XRP price for April 30, 2026

Trezor Academy Releases Documentary on Africa’s Bitcoin Economy, Opens Education Donations

Ripple Price Prediction: Will the CLARITY Act Trigger a Repricing Event for XRP?