Hyperliquid's success and hidden dangers

I've been really busy lately and can't write a 10,000-word research report any more. I'll try to change my writing style and just state my opinions and reasoning. Please forgive me, dear readers.

1. Research Background

I have recently researched almost all the Perps (perpetual trading platforms) on the market. The five-fold growth of the hype market proves once again that when I first researched it last year, I still overlooked its core value.

Moreover, recently aster, antex, dydxV4, and even Sun Ge's sunPerps, which shook the track, have gradually brought the Perps track into a period of explosive growth.

Furthermore, major exchanges are vying to list Hyper and its perpetual trading capabilities. Yesterday, news broke that Metamask, following Phantom, is planning to integrate Hyper's perpetual trading capabilities. Circle has also become a validator, addressing concerns about its core decentralization. Hyperliquid itself is also striving to improve its openness, particularly with the gradual rollout of HyperEVM and HIP2/3/4.

1.1 Three Elements of the New Track

At this point, Perps basically has the three key elements of a new track.

In fact, if we look back at any huge track wave in history, we can see that it is often the new leading platform, new wealth opportunities, and new narrative background. The trend gathering will bring about peaks, while the subsequent platform's airdrop strategy, the gradual development of platform complexity, and the decline in user perception of freshness will gradually bring about troughs.

This process has actually gone through many waves. The typical scenarios are as follows. The following modules have been analyzed in the previous public account articles of "Fourteen Gentlemen". If you are interested, you can check it out yourself:

- The ICO craze of 2017 was centered on the CEX platform. It's a basic necessity, uncontroversial, and many are doing very well now.

- In the summer of DeFi in 2021, the corresponding platforms are Uniswap, lending and stablecoins, as above.

- NFTs, which have been around for 22 years, actually have protocols that existed long before, but only reached their peak thanks to OpenSea. The root of this was pricing through transactions, which then led to dissemination based on price. Its decline stemmed from arrogance, with its airdrop strategy and royalties leading to a death spiral of price increases, a self-inflicted consequence.

- The 23-year-old inscription, corresponding to the platform Unisat, was ultimately driven by short-sightedness. At its peak, it focused on asset issuance, not application development, resulting in a short lifespan for its narrative. When other new narratives emerged, RWA and perps dominated attention, hindering the recent Alkanes and BRC2.0 from regaining their popularity. This is a self-inflicted failure.

- The 24-year meme and the corresponding pump platform, as well as this year's dark horse Axiom, have made this wave exceptionally long-lasting. This is due to the advantages of the chain itself in terms of transactions, the constant influx of people who are interested in trading, and the new users brought by the wave of compliance, which has enhanced the life cycle.

- Finally, in 25 years, there are both RWA (focused on stocks) and Perps (led by hyperliquid).

2. Understanding the key steps in the development of hyperliquid

2.1 Current Development Status

Objectively speaking, the system remains relatively centralized, theoretically capable of being disrupted by unplugging the network. Furthermore, hacker funds are siphoned off, creating significant obstacles for many exchanges in terms of compliance and attracting significant attention. However, the data is highly contradictory.

Hyperliquid currently has about 10,000 to 20,000 daily active users, out of a total user base of about 600,000. A core group of 20,000 to 30,000 of these users contributes nearly $1 billion in revenue, a significant portion of which comes from the United States.

The cumulative trading volume has exceeded 3 trillion US dollars, and the average daily trading volume has reached nearly 7 billion US dollars.

Currently supports Perps trading of more than 100 assets.

Looking at his data in this way, I can only say that it is really great. Although the number of users seems small, they are the group that can make the most money.

2.2 Major Updates and Interpretations

The specific timeline is as follows

- March 25: HyperCore and HyperEVM were connected, theoretically allowing users to trade core tokens from the EVM (trading only at the time).

- April 30: Launched the read precompile feature, enabling HyperEVM smart contracts to read state from HyperCore.

- May 26: Small block time halved to 1 second, increasing the throughput of HyperEVM.

- June 26: The HyperEVM block was updated to remove the previous ordering of only published orders to improve integration with HyperCore.

On July 5, HyperEVM updated a new precompiler called CoreWriter. This enables HyperEVM contracts to be written directly into HyperCore, including functions such as placing orders, transferring spot assets, managing treasury bonds, and staking HYPE.

Recently, Builder core and Hip4 have also entered the data prediction market. This step of entry was completely unexpected by the market. This also means that the founders have very unique ideas in thinking about the pain points of the industry, which often leads to polarization of the platform.

How do you understand this series of updates?

First, compared to last year, Hyperliquid now has open core order operation capabilities.

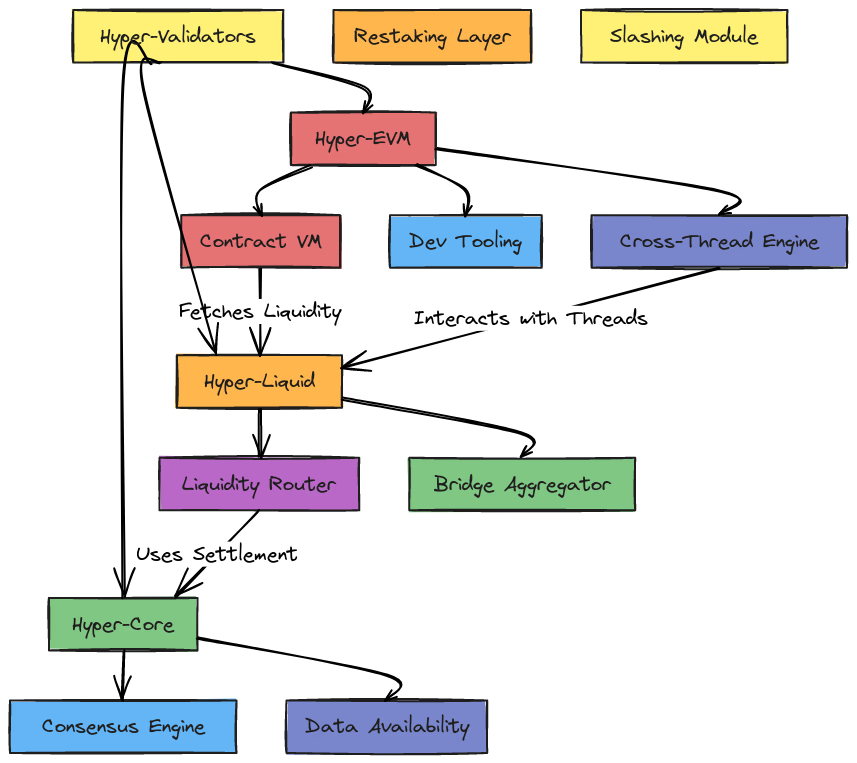

HyperEVM

In particular, the dual-chain architecture based on EVM has an outrageous logic. Under the premise that HyperCore is not open (cannot be deployed), a large number of pre-compiled contracts are added through HyperEVM and connected to HyperCore. In theory, it has the access basis of wallets (phantom, metamask) and exchanges, and can theoretically realize EVM transaction operations to execute Core's order asset trading and other capabilities.

The official picture shows the positioning of hyperEVM in the system

It can be seen that HyperCore and HyperEVM writes and reads are uniformly confirmed by HyperBFT. The specific mechanism of the validator's confirmation information mechanism is not public, and there is no cross-chain bridge or delayed synchronization.

The dynamics that can be seen through on-chain transactions are that HyperEVM can affect HyperCore by executing writes through the system contract (0x333…3333, CoreWriter.sendAction(...)), which can perform order placement, liquidation, and lending operations.

The status (of the previous block) fed back by HyperCore can be read by the smart contract of HyperEVM.

- User data — positions, balances, and vault information

- Market Data — Mark Price and Oracle Price

- Staking data — delegation and validator information

- System data - L1 block count and other core metrics

The information is essentially received by the EVM system contract, which generates corresponding receipts or events and records them. And in the EVM, the precompiled contract (0x000…0800) can call perp positions or oracle price (oraclePx)

Secondly, the implementation of hip2 and hip3 is changing the platform positioning of Hyperliquid.

Hyperliquidity

This is an on-chain liquidity mechanism built into Hypercore.

It automatically places buy and sell orders based on the current price of the token, maintaining a narrow spread of approximately 0.3% without manual intervention.

This mechanism allows for native-level liquidity insertion operations built into the block logic without AMMs or third-party bots.

For example, when the PURR/USDC spot market launched, Hyperliquidity immediately issued seed transactions with initial depth, allowing real trading before normal user liquidity arrived.

Builder core

This mechanism is highly valuable for the future, allowing DeFi builders (developers, quantitative teams, and aggregators) to collect additional fees as service revenue when placing orders on behalf of users. The application scenario for this system is clear, and it represents a move to open up profits and embrace ecosystem co-construction.

**Quantitative strategy hosting, **The quantitative team helps users place perp position orders and collects management fees through builder fees, forming a compound profit model of "revenue sharing + builder fee"

**Aggregators/transaction routers,** such as 1inch and Odyssey, integrate perp trading services on Hyperliquid and can charge builder fees as a routing revenue model.

The initial launch has already brought over 10 million US dollars in dividend income to some projects, which shows the effect of hyper funds being deeply deposited at the platform level.

In fact, the issue of opening up depth is not just Hyper. The previous Uniswapv4 also wanted to do this through hooks, but v4 did not take off, and most users are still accustomed to v2 and v3.

This may be the influence of having less historical baggage and stronger centralized decision-making.

3 Summary and Comments

3.1 There are many advantages. Let’s go through them one by one.

Hyperliquid's primary advantage was its strong early product capabilities, which stemmed from addressing two user pain points:

- The trading needs of non-compliant users are actually even more rare in this year's wave of compliance.

- Advanced trading users demand high leverage and high transparency. The former brings KOL exposure, while the latter is often ignored by market incumbents, that is, the dark under the light, thus catching many CEXs off guard.

The second is the team background itself. Its biggest advantage here is that it has a small number of people, so the communication gap, wear and tear, and labor efficiency are all very high. With an overall staff of more than a dozen people, excluding 3-4 product operation BDs and deducting the front-end and back-end, it means that only 3-4 people can build a high-performance chain of 20Wtps.

Compared with many blockchain teams of traditional large companies, which can also produce a lot of palace fighting dramas, it is much better.

In the background, his market maker foundation started in 2020 actually brought good initial depth. He also felt in many details that his matching logic and other order book systems are not simply settled gradually by time and amount.

However, the data is insufficient, so I will supplement it later when I do comparative analysis of multiple Perps.

Then there's the trend.

General projects need to adapt to the market, but when a platform reaches its peak popularity, the market can adapt to it.

This is the treatment Hyperliquid is receiving now.

On the one hand, the openness of the aforementioned updates creates space for diverse ecosystems to enter. This contrasts with many previous platforms, which often prioritized doing everything themselves, reaping all the benefits, single-handedly criticizing OpenSea, and even imposing mandatory royalty systems, forcing the market to follow the leading platform. Each of these platforms incurs high, fixed costs, interfering with the flow of goods and affecting market pricing, ultimately becoming a family heirloom.

In Hype, he opened up EVM and all kinds of DEX PEPS APIs, so soon a bunch of derivatives appeared on the market.

Hyperliquid's generosity can also be seen in the airdrop. It was impossible for it to take the compliance route from the beginning.

Therefore, he will not try to embrace the so-called expectations of going public, so he will naturally release the profits. Then he will pledge the hype back through the HLP mechanism, release the profits and make profits again, so that the official tokens can be dispersed and the market will gain the most valuable decentralized evaluation and reputation.

Its openness has attracted market acclaim. Phantom first integrated its perps capabilities from the perspective of a decentralized wallet. This is not difficult, mainly due to the large amount of adaptation and development costs. Recently, there are rumors that Metamask is also integrating it.

From this we can also see that those decentralized wallets that have not been updated for more than half a year have also learned to seize the annual narrative after missing the inscription.

Finally, he pushed for the introduction of giants such as Circle to join as validators to bring decentralized security and fill his decentralization gap, so that highly compliant CEX platforms also had the opportunity to access.

3.2 Disadvantages

After the most challenging initial phase, the next issue is compliance. Even pure DEXs like Uniswap are embracing compliance, not to mention the European and American Hyperliquid, whose users have also made their fortunes. If a platform is deemed non-compliant or otherwise severely errs, existing CEX/Wallet partnerships will be severed, and former allies will part ways.

In addition, the subsequent development of this system will also face the problem of development complexity. Most projects become more and more complicated as they are written, and it is difficult to simplify them and return to the first principles. In the end, novice users cannot understand how to use them and lose fresh blood.

Finally, there's the single-point risk. The current claimed 20Wtps, if accessed by multiple global platforms, would create numerous information inconsistencies, placing immense pressure on the core hyperCore module. Building this high performance takes time. The official market maker background may not be able to handle the volume, and if multiple outages trigger liquidation issues (similar to the short squeeze incident in March), this could lead to significant downtime.

The reputation that is accumulated with great difficulty is inherently fragile.

You May Also Like

China’s EV insurance business is losing a lot of money because repair costs are too high

Shiba Inu Price Forecast: Why This New Trending Meme Coin Is Being Dubbed The New PEPE After Record Presale