Moody’s Stock Trades at $450 While Streets Target $537. Is It a Buy Now?

Key Takeaways for Moody’s Stock as of June 2026

- Analysts rate Moody’s stock 12 buys / 7 holds / 0 sells with a mean target of $537, implying around 19% upside from the current price of $450.

- TIKR’s mid-case model values Moody’s at around $707 by December 2030, implying around 57% total return, or roughly 11% annualized.

- Moody’s Analytics ARR reached $3.6 billion in Q1 2026, up 8% year over year, with KYC growing 13% and management guiding a reacceleration into mid-teens growth through the back half of 2026 as the new Moody’s for Compliance product builds its first renewal cohort.

Track Moody’s EBITDA, ARR, and full forward estimates on TIKR and see where Street consensus sits before the next earnings call. Access MCO financials on TIKR for free →

Moody’s Q1 2026 EBITDA Climbs 11% as the AI Distribution Flywheel Builds Behind MCO Stock

MCO Stock Q1 2026 Earnings in USD (TIKR)

MCO Stock Q1 2026 Earnings in USD (TIKR)

Moody’s Corporation (MCO) delivered $2.08 billion in revenue for Q1 2026, up 8% year over year, while EBITDA reached $1.11 billion, up 11% with margin expanding roughly 150 basis points to 53.2%. Rated issuance surpassed $2 trillion for the first time, led by near-record investment-grade volumes including more than $100 billion in hyperscaler-related financings.

What the headline numbers do not surface is the operating leverage building underneath. MIS delivered a 66.7% adjusted operating margin by processing that record issuance without proportional headcount growth, supported by AI-enabled workflow automation in financial statement spreading and pre-committee analytical prep.

CEO Rob Fauber addressed the dynamic directly on the Q1 call: “The AI enablement really picked up in the back half of last year… it’s not only about efficiency. It’s also going to be about insight as well.” Those efficiency gains are already visible in the margin print but not yet fully annualized.

On the Moody’s Analytics side, adjusted operating margin reached 32.5%, up 250 basis points year over year, with full-year guidance of 34% to 35% and a medium-term target of mid-to-high 30s by end of 2027. Annual Recurring Revenue ended Q1 at $3.6 billion, up 8%, with KYC growing 13%, the Lending Suite growing in the high teens, and trailing twelve-month retention holding at 95%.

The structural layer is distribution. Over the past two quarters, Moody’s embedded its data into Claude, ChatGPT Enterprise, Microsoft 365 Copilot, and Amazon Q through Model Context Protocol integrations on a bring-your-own-license basis. Fauber noted that financial institutions are already in active pilot discussions for agent-ready enterprise licenses structured to expand usage across entire divisions.

Those conversions, if they build through the year, represent commercial uplift not yet reflected in ARR.

Moody’s just reported its strongest MIS quarter ever while expanding MA margins 250 basis points. See the full forward EBITDA trajectory for MCO on TIKR for free →

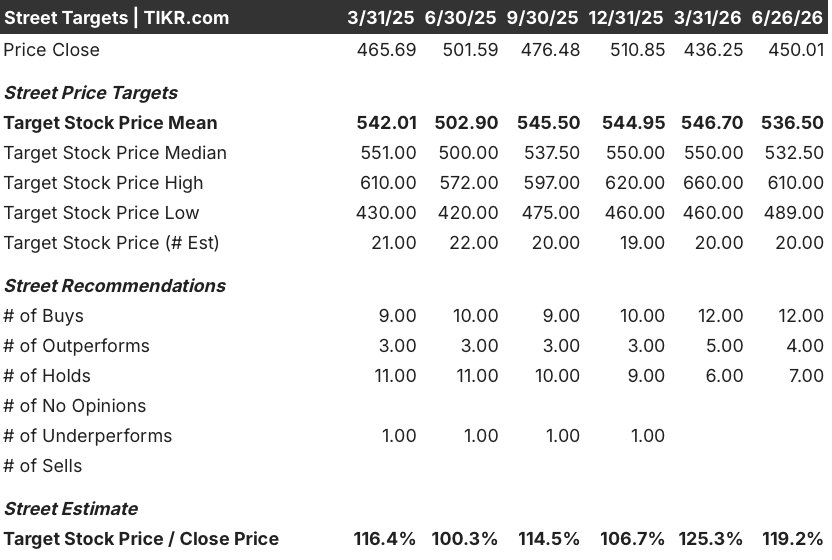

Wall Street Carries 12 Buys on Moody’s Stock With a $537 Mean Target

Street Analysts Target for MCO Stock (TIKR)

Street Analysts Target for MCO Stock (TIKR)

As of late June 2026, 20 analysts cover Moody’s stock with 12 buys, 4 outperforms, and 7 holds. The mean price target sits at around $537, with the high end reaching $610 and the low end at $489, implying around 19% upside from the current price of $450.

That distribution reflects broad institutional conviction on the fundamental quality of the franchise with some caution anchored to near-term MIS cyclicality and the still-early monetization stage of the AI distribution partnerships.

Wall Street Expects Moody’s Stock EBITDA to Sustain Above 50% Margins Through 2027

MCO Stock EBITDA and EBITDA Margins Actuals & Estimates (TIKR)

MCO Stock EBITDA and EBITDA Margins Actuals & Estimates (TIKR)

EBITDA came in at $1.11 billion in Q1 2026, up 11% year over year, with a 53% margin, up 149 basis points from the prior year.

Street consensus projects around $1.08 billion for Q2, $1.12 billion for Q3, and $1.01 billion for Q4, reflecting typical MIS seasonality. That puts full-year 2026 EBITDA near $4.3 billion with margins above 50% in every quarter. Into Q1 2027, consensus reaches roughly $1.20 billion with margins approaching 54%.

The open question is whether the second-half MIS moderation is a timing effect or the start of something more durable. Bulls point to the $2 trillion Q1 issuance print, a live M&A backlog, and structural funding needs across infrastructure and private credit. Bears note that speculative-grade issuance remains selective, hyperscaler debt is front-loaded, and any sustained risk-off window would compress the back half before MA margin expansion can offset it.

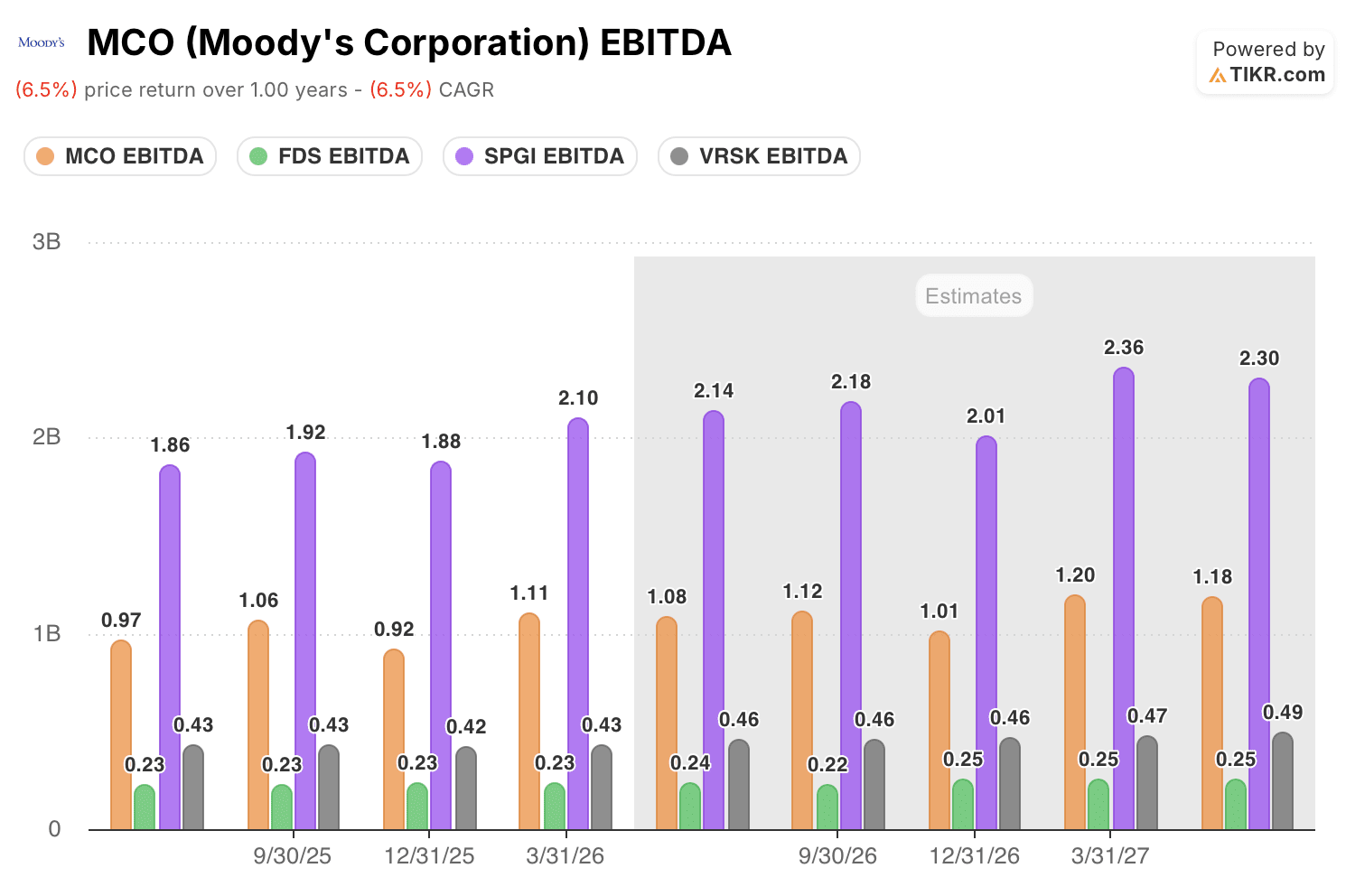

Moody’s Stock Generates More EBITDA Than Every Peer Except S&P Global

MCO Stock EBITDA vs Peers (TIKR)

MCO Stock EBITDA vs Peers (TIKR)

Moody’s posted $1.11 billion in EBITDA for Q1 2026, sitting second only to S&P Global (SPGI) at $2.10 billion among financial data peers. Verisk (VRSK) came in at $430 million and FactSet (FDS) at $230 million, putting both at a fraction of Moody’s quarterly output.

That gap holds through the forward estimates. Street consensus projects Moody’s reaching roughly $1.20 billion in EBITDA by Q1 2027, compared to around $2.36 billion for S&P Global, $470 million for Verisk, and $250 million for FactSet. Moody’s is growing EBITDA at around 8% into that quarter, faster than Verisk and FactSet on a year-over-year basis, while narrowing the scale discount to S&P Global.

The competitive implication is straightforward: Moody’s is the only peer combining ratings-cycle leverage with a subscription analytics segment expanding margins by 250 basis points a year. That dual-engine profile does not exist at Verisk or FactSet, and S&P Global carries a materially higher absolute EBITDA base but faces similar MIS cyclicality without the same MA margin expansion runway.

TIKR’s $707 Target on MCO Stock Holds If Operating Leverage Compounds Through 2027

TIKR’s mid-case model values Moody’s at around $707 by December 2030, implying around 57% total return from the current price of $450, or roughly 11% annualized over 4.5 years.

MCO Stock Valuation Model Results (TIKR)

MCO Stock Valuation Model Results (TIKR)

At 11% annualized from a business with 95% retention, expanding margins at both MIS and MA, and two secular growth drivers in private credit and AI infrastructure financing, Moody’s stock is not structurally expensive at $450.

The path to that target rests on what Q1 already showed: EBITDA margin expanded at both segments simultaneously. If MA ARR reaccelerates as guided and MIS absorbs any second-half softness without a full guidance cut, the margin trajectory TIKR models to 2030 is achievable on existing product cadence alone.

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Moody’s Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Moody’s Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MCO stock on TIKR for Free →

You May Also Like

Bitcoin Faces Volatile Week As Geopolitical Risks And Fed Signals Keep Traders On Edge: QCP Capital

AI spending boom accelerates as Big Tech pours trillions into infrastructure