Netflix Will Trade at This Price in 2028

The post Netflix Will Trade at This Price in 2028 appeared first on 24/7 Wall St..

Netflix (NASDAQ:NFLX) is the streaming business everyone thought had matured, yet management is still raising the ceiling. Co-CEO Greg Peters told investors Netflix accounts for only 5% of TV view share globally, with “tons of room for growth still ahead of us.”

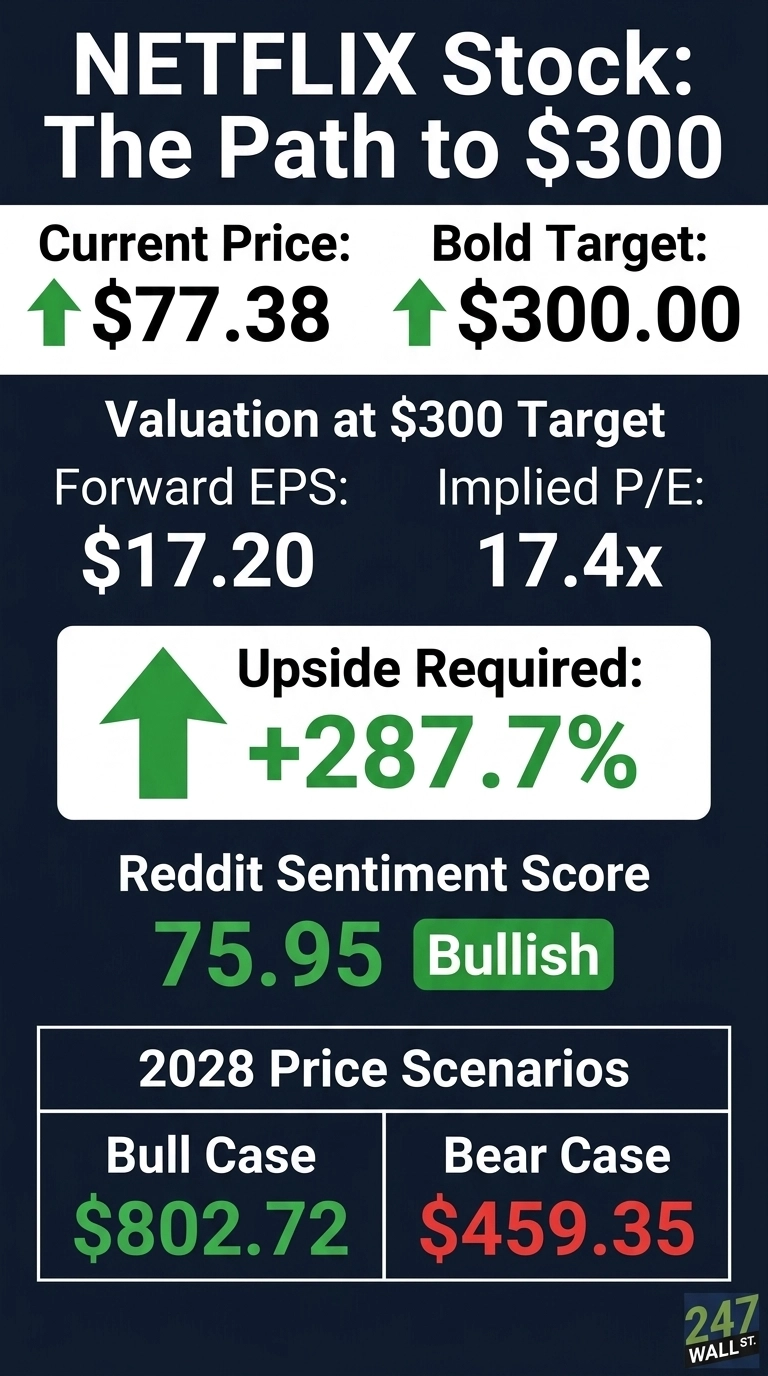

Advertising is doubling to $3 billion in 2026. Free cash flow guidance was just raised to $12.5 billion. So why are shares down 17.47% year to date? More importantly, can NFLX reach $300 by 2028?

What’s Holding Netflix Back Right Now

The pain is real. NFLX is off 4.79% in the past week, 13.38% over the past month, and 36.69% over the last year.

Two things are weighing on the stock. First, Q1 2026 EPS of $1.23 missed the $1.345 consensus by 8.55%, even with a $2.80 billion Warner Bros. termination fee padding net income.

Second, the walked-away Warner Bros. deal left investors confused about strategy. Add in a beta of 1.491 and shares are now 15% below the 52-week high of $134.12. The selling has been mechanical.

Wall Street Sees 47% Upside. Our Model Sees Much More

The Street is constructive. The analyst consensus target sits at $114.15, with 8 Strong Buys, 29 Buys, 13 Holds, and zero sell ratings. Our base case is $284.54 by 2028, a 267.72% total return with a 90% confidence score. The bear case still pencils to $459.35 by year-end 2028.

With 74% of analysts bullish and earnings growing 86.4% year over year, I think the Street is anchoring to a depressed multiple and underestimating operating leverage. The disconnect between consensus and fundamentals is the opportunity.

24/7 Wall St.

24/7 Wall St.

The Path to $300 Per Share

Let’s do the math. Reaching $300 from today’s price of $77.38 would require a gain of 287.7%. With forward EPS of $17.2, a $300 price implies a forward P/E of 17x. Our base case of $284.54 already implies 5x, meaning the bold target requires roughly 0.9x of incremental multiple. That is trivial.

Here is the compression story. Shares trade at a current forward P/E near 5x against $17.2 in projected earnings power. Even at a 17x multiple (well below the current 24x forward P/E on TTM EPS), $300 is reachable.

The 247Factor adjustment of 1.107 reflects strong analyst consensus (+0.044), earnings acceleration (+0.03), and bullish sentiment.

Catalysts are real: ad revenue doubling to $3 billion in 2026, the World Baseball Classic driving Japan’s largest single sign-up day ever, and Co-CEO Ted Sarandos noting Netflix is “ramping up our sports events globally.” The primary risk is content amortization and FX compressing margins in front-loaded quarters.

Where Netflix Trades Today vs Its Earnings Power

At $77.38, shares sit near the 52-week low of $75.01, far below the high of $134.12. The trailing P/E is about 25x while operating margins are guided to 31.5% in 2026, up from 29.5% in 2025.

NFLX has returned 724.95% over the past 10 years. That kind of compounding requires execution Netflix has actually demonstrated. The current valuation looks cheap against forward earnings power.

Is $300 Realistic? Here’s My Take

Reaching $300 by 2028 requires a 287.7% gain. That sounds extreme, but the bear case still gets us to $459.35.

Three things must happen: ad revenue must hit $3 billion in 2026 and keep doubling, operating margins must clear 33%, and the live sports flywheel must deliver Japan-style sign-up events globally. A protracted recession or content cost re-acceleration would derail it. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Netflix could reach $300 in 2028.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Netflix didn’t make the cut. Grab the names FREE today.

The post Netflix Will Trade at This Price in 2028 appeared first on 24/7 Wall St..

You May Also Like

Bitcoin Drop Sparks $700M Liquidation Wave As Leverage Gets Flushed

A 68-Year-Old’s Roth Conversion Cost Him the $6,000 Senior Deduction That Was Shielding His Social Security

Datavault AI Expands WiSA Wireless Audio Technology Into Goldhorn Home Systems in China