Congress Moves to Close Bitcoin Wash Sale Tax Loophole, Redirect Break to Stablecoins

A bipartisan congressional proposal would close the tax loophole that lets Bitcoin traders sell at a loss and immediately repurchase to claim a deduction, while carving out a new $200 tax exemption exclusively for regulated stablecoin payments.

The Digital Asset PARITY Act, released as a discussion draft on December 20, 2025, was introduced by Rep. Max Miller (R-OH) and Rep. Steven Horsford (D-NV). The bill would rewrite Section 1091 of the Internal Revenue Code to apply wash-sale and constructive-sale rules to actively traded digital assets and their derivatives.

Under current law, the wash-sale rule prevents stock investors from claiming a tax loss if they repurchase the same security within 30 days. That restriction has never applied to cryptocurrency. Bitcoin holders can sell during a drawdown, book the loss against their taxable income, and buy back seconds later with no penalty.

The PARITY Act would eliminate that gap. If enacted, Bitcoin and other crypto assets would fall under the same 30-day wash-sale window that governs equities, ending a tax-loss harvesting strategy that retail traders and institutional funds have relied on for years. The scale of the practice remains unquantified by the IRS, though crypto media have described it as “widely used.”

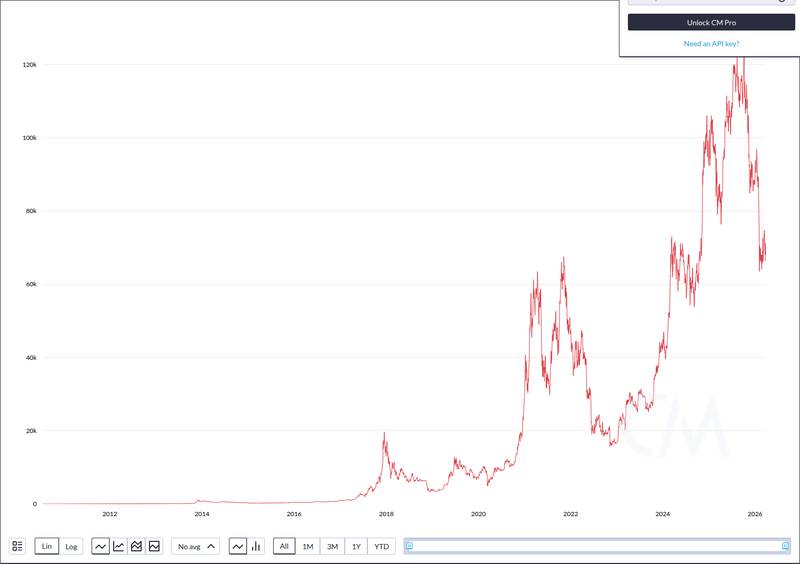

Bitcoin traded at $66,253 at press time, down roughly 47% from its all-time high of $126,080 set in October 2025. In an environment where the Fear & Greed Index sits at 9 (Extreme Fear), many holders are sitting on unrealized losses, making the wash-sale exemption particularly valuable right now.

CoinMarketCap chart illustrating the price backdrop referenced in this article on bitcoin.

CoinMarketCap chart illustrating the price backdrop referenced in this article on bitcoin.

Regulated Stablecoins Get the Tax Break Bitcoin Loses

The bill does not simply tighten the rules across the board. It simultaneously creates a $200 de minimis tax exemption for transactions made with federally regulated payment stablecoins. Under this provision, everyday stablecoin purchases would not trigger gain-or-loss recognition, a relief that Bitcoin and other volatile crypto assets would not receive.

The distinction signals a clear policy preference. Congress appears to view regulated, dollar-pegged stablecoins as legitimate payment instruments deserving tax simplicity, while treating Bitcoin and similar assets as speculative investments subject to tighter compliance. This framing aligns with the broader push behind the GENIUS Act and STABLE Act, both advancing through Congress in 2026 to establish a federal stablecoin regulatory framework.

Only stablecoins meeting federal regulatory standards would qualify for the exemption. The bill text specifies “regulated payment stablecoins,” excluding algorithmic or unregistered tokens. For holders using stablecoins to buy coffee or pay for services, transactions under $200 would carry zero tax reporting burden.

The two-sided structure of the bill, closing one loophole while opening another, has drawn criticism. The Bitcoin Policy Institute characterized the approach as creating a “two-tier tax regime” that disadvantages proof-of-work systems.

CoinMetrics on-chain context supporting the network-flow discussion around bitcoin.

CoinMetrics on-chain context supporting the network-flow discussion around bitcoin.

Staking Gets Relief, Mining Does Not

Beyond the wash-sale and stablecoin provisions, the PARITY Act creates an elective deferral framework for staking rewards, addressing the “phantom income” problem where validators owe taxes on tokens received before they can sell them. However, miners operating under proof-of-work consensus are excluded from this deferral.

The bill also allows mark-to-market elections for digital asset traders and dealers, extends securities-lending tax rules to crypto, and modernizes charitable contribution rules for digital assets. These provisions represent the most comprehensive bipartisan crypto tax reform effort Congress has produced to date.

Rep. Miller framed the legislation as overdue modernization. In a statement accompanying the draft, he said the bill “brings clarity, parity, fairness, and common sense to the taxation of digital assets” while protecting consumers and strengthening compliance.

What Bitcoin Investors Face Next

For traders who rely on year-end tax-loss harvesting, the practical impact is significant. If the wash-sale provision passes, selling Bitcoin at a loss and repurchasing within 30 days would disallow the loss deduction, the same restriction that has governed stock investors for decades. Year-end portfolio rebalancing strategies would need to account for the waiting period.

The bill remains a discussion draft gathering stakeholder feedback and has not been formally introduced. Rep. Miller has stated he believes the broader legislation can advance before August 2026, giving the crypto industry roughly four months to shape its final form. The recent wave of institutional expansion into crypto services adds urgency to the tax clarity debate.

Bipartisan co-sponsorship from Miller and Horsford improves the bill’s chances of advancing through committee, though the PoW exclusion from staking relief could become a sticking point. The Bitcoin Policy Institute has formally urged Congress to extend equal treatment to miners, and industry lobbying efforts are expected to intensify as the August target approaches.

With Bitcoin down sharply from its highs and liquidation events hitting leveraged positions, the timing adds pressure. Traders who might otherwise harvest losses freely during this drawdown face the prospect of that strategy disappearing. Whether Congress moves fast enough to affect 2026 tax planning depends on committee action in the coming weeks.

The next concrete milestone is formal introduction of the bill text. Until then, the discussion draft remains open for industry stakeholders tracking the legislative calendar to submit feedback and push for amendments before markup begins.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency and digital asset markets carry significant risk. Always do your own research before making decisions.

추천 콘텐츠

Hallmark Announces 2025 ‘Countdown To Christmas’ Dates, Movies, And Fan Events

Sources: The Senate hearing for Federal Reserve Chair nominee Warsh is expected to take place as early as the week of April 13.